Navigating Older Roofs & Homeowners Insurance Coverage Q&A

Your roof is one of the most important components of your home, protecting everything (and everyone) inside from the elements. As a homeowner, it is crucial to have sufficient homeowners insurance to protect your roof in case disaster strikes. You may have heard of the “10-year rule” when it comes to roofing, but what exactly does that mean? Does your roof expire after a decade? This Q&A blog post explains everything you need to know about the “10-year rule.” To give you the most accurate information, we spoke with several insurance experts who provided their insights for this post. Let’s dive into the common questions homeowners have about this important roofing topic.

Q: What is the “10-Year Rule” in Roofing? How does it impact Homeowners Insurance Coverage?

A: The “10-year rule” as it pertains to homeowners insurance commonly refers to the practice in which insurers reduce coverage or even deny claims for roofs older than 10 years, often switching from Replacement Cost Value (RCV) to Actual Cash Value (ACV) for older roofs.

Q: Actual Cash Value (ACV) vs. Replacement Cost Value (RCV): What’s the difference?

A: ACV (Actual Cash Value) covers the depreciated value of your damaged property, meaning what it’s worth today. RCV (Replacement Cost Value) pays to replace your damaged property with a new, similar item, without deducting for depreciation. RCV generally offers more coverage but comes with higher premiums.

Q: How Does a roof’s age (around 10 years+) trigger a shift from RCV to ACV?

A: Many homeowners insurance policies initially offer Replacement Cost Value (RCV) coverage for your roof. With RCV coverage, if your roof is damaged by a covered peril (like wind or hail), the insurance company pays for the cost to replace it with a new, comparable roof at current prices, without deducting for depreciation.

As a roof ages, particularly once it reaches a certain benchmark, like 10, 15, or sometimes 20 years old, many insurance companies will switch the coverage for the roof to Actual Cash Value (ACV). With ACV, the payout for a damaged roof is based on its depreciated value at the time of loss. This means that your insurance company calculates what your old roof was worth right before it was damaged, factoring in its age, wear and tear, and pays you that amount minus the deductible.

Q: What happens when my policy shifts from RCV to ACV and what should homeowners watch out for?

A: The difference is substantial. According to Patrick Caruso, President of Caruso Insurance Service: “The key language homeowners need to watch for is “actual cash value” versus “replacement cost” coverage on their dwelling. When policies shift to ACV for roofs over 10 years, you’re looking at depreciation calculations that can leave homeowners paying 60-70% out of pocket for a roof replacement. I’ve had clients with 12-year-old roofs receive only $8,000 on a $25,000 claim.”

Q: How do insurance companies determine what an ACV policy will pay out?

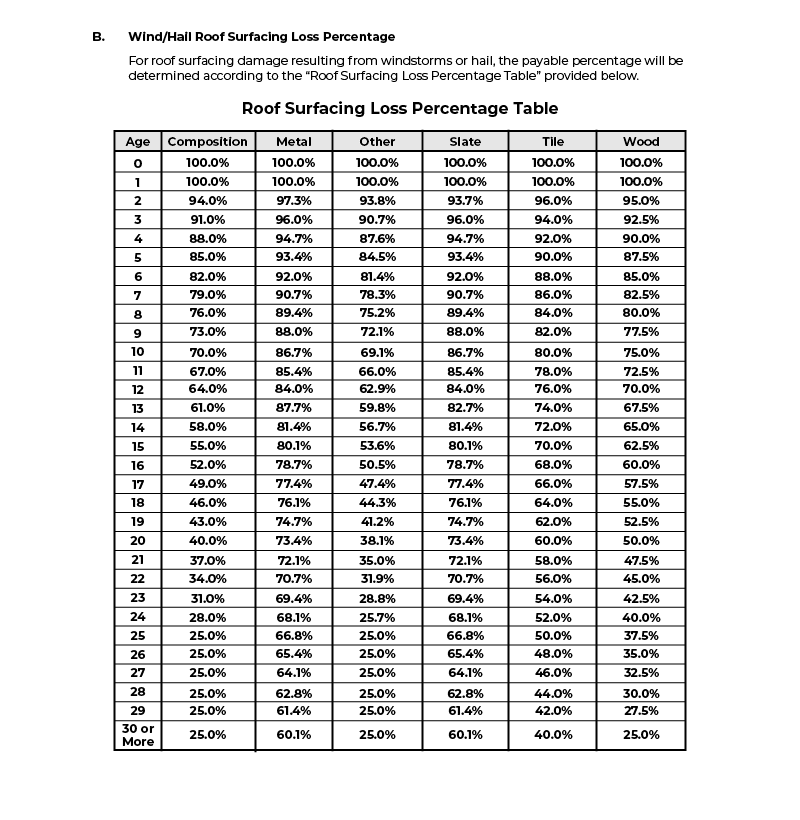

A: Many insurance providers use what is called a roof payment schedule, which establishes a predetermined depreciated payout for roof damage based on its age and material, rather than its full replacement cost. We’ve included an example of a roof payment schedule below to help you visualize how ACV payouts can work:

Q: What are the long-term implications of the “10-year rule” for homeowners?

A: There are several important implications homeowners should be aware of, like rising deductibles, an increase in out-of-pocket costs, and how this may impact the housing market. Many insurance experts recommend prioritizing proactive home maintenance, including roof maintenance to help manage rising costs.

Ashley Beeman from BIG Insurance Group explains “I personally think this will have a negative effect on the housing market because buyers who are armed with this information will not want to purchase a home with a roof that is close to 10 years old, which could cause the home to sit on the market for longer. Another important thing for homeowners to be aware of is rising deductibles. Percentage deductibles are becoming the standard in Colorado, although there are a few companies that do not yet require them. The percentage is based on your coverage amount, so if your home is covered for $600,000 and you have a 1% deductible, you will be responsible for $6,000 before your insurance company will pay out on a claim. Many companies are changing deductibles at renewal, so it is crucial to read the policy language sent to you yearly.”

Andrew Harris, Liberty Insurance President, claims “The long -term implications for homeowners are significant, primarily leading to higher out-of-pocket expenses and a greater emphasis on proactive roof maintenance. This shift demands homeowners become more deeply engaged in understanding their policy nuances and potential coverage gaps before a claim arises, making preventative care more crucial than ever.”

Q: What is the reason for these insurance changes and “10-year rule”?

A: The general consensus among insurance experts is clear: These policy shifts are driven by a combination of factors, primarily the rising costs of labor and building materials, alongside the escalating frequency and intensity of catastrophic weather events.

Ashley Beeman from BIG Insurance Group adds “Insurance companies have not been profitable in Colorado in recent years due to the severity of weather and the rising cost in building materials, which in turn leads to higher payouts. All carriers who are still writing business in Colorado had to make changes to be able to stay in the state. Many have raised deductibles, changed underwriting guidelines, and changed coverages/deductibles. Some have even put quotas on the amount of business each agent can write. This is also why we have seen such dramatic premium increases since 2023.”

Q: Is the “10-year rule” specific to Colorado? Are other regions affected?

A: The “10-year rule” impacts country and state regions that are frequently subject to catastrophic weather events, but some insurers are noting a broader change. In Colorado, for example, the “10-year rule” is more common in specific areas that are prone to hail damage. Ashley Beeman from BIG Insurance Group elaborates “The Western Slope is less at risk for this, since they do not get the same kind of hail that places like the Front Range do. Not all companies are making this change, so some people are grandfathered into having the full replacement of their roof, even if it is greater than 10 years old.”

Liberty Insurance President, Andrew Harris, states “As a PIA National Agent of the Year, and with my involvement in Marsh Berry’s CONNECT program, I’ve seen these changes across the industry, not just regionally. Through my work on the National Provider Council for Selective Insurance, we’ve observed these trends emerging more broadly, particularly across the Northeast and Mid-Atlantic states, as insurers adapt to evolving risk profiles.

Patrick Caruso, President of Caruso Insurance Service in California adds “As an independent agent working with multiple carriers daily, I’m seeing this trend accelerate dramatically in our Corona, CA market and throughout Southern California. Farmers Insurance and Allstate have been the most aggressive in implementing these restrictions, particularly after the recent wildfire seasons drove up their claim costs by over 40% in our region.”

Q: Is My Roof Really “Expired” After 10 Years?

A: The short answer is no. The expected lifespan of your roof depends on your roof type and the quality of the installation of it. Different roof materials have different average expected lifespans. For example, asphalt roofs last an average of about 20 years. However, stone-coated steel, clay and concrete tile, and synthetic composite roofing materials can last up to 50 years or longer. As a homeowner, it’s important to carefully consider the quality and average expected lifespan of a roofing material when choosing a new roof.

Conclusion:

While the “10-year rule” isn’t a set expiration deadline for your roof, it serves as a critical marker for understanding your homeowners insurance coverage. By being proactive and informed, you can avoid costly roofing surprises and ensure your home remains safe for years to come.